The inauguration of only the second U.S. president to win two non-consecutive terms (Grover Cleveland was the first) is historic by a host of measures. Starting a second term of office with the president’s party controlling both houses of Congress gives rise to expectations of an opportunity to move the goalposts on what worked well, and succeed on aims that fell short the first time around.

However, the economy is in a very different place than it was eight, or even four years ago. Will a new economic cycle and a vastly different interest rate environment change plans and outcomes?

Let’s get into the data:

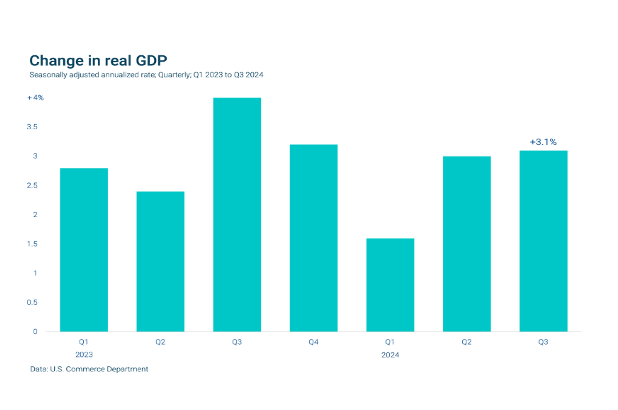

GDP is up, inflation is holding steady, and the labor market remains solid. The Federal Reserve cut rates three times in 2024, for a total 100 basis point decrease in the key short-term rate, to a target range of 4.25%-4.5%. Two more rate cuts are expected in 2025, based on the predictions of the Fed’s dot plot. The Fed has for now delivered a soft landing, and is in a position to adeptly navigate further rate cuts while keeping the economy blooming.

So with a strong economy, the uncertainty of the election removed, and a pro-business regime about to take power, why is the bond market looking so spooked? The yield on the 10-year U.S. Treasury notes climbed to 4.71% as of January 8th, up over 100 basis points from its level in mid-September.

Longer-term rates in the bond market correspond to views on inflation, the strength of the economy, and other factors. Rates going up signals that investors are demanding to be compensated for additional risk.

While the potential for a radical expansion of the United States’ footprint from Greenland to Panama is great copy, it’s probably not the reason for bond market jitters. Closer to home, the impact of bigger deficits resulting from tax cuts may be the culprit. While increased tariff revenue could shrink the deficit, it would likely also bring inflation back to life, which could result in the Fed raising rates and tamping down the economy.

For now, all the pieces of the new agenda are still being determined. There will be trade-offs, and likely some traditional horse trading between and amongst the parties.

Chart of the Month: GDP ends the year on a high note

· The S&P 500 was down 2.50% for the month

· The Dow Jones Industrial Average fell 5.27%

· The S&P MidCap 400 decreased 7.29% for the month

· The S&P SmallCap 600 was down 8.12%

Source: S&P Global. All performance as of December 31, 2024

The Magnificent 7 group was 53.1% of the S&P 500’s total return for 2024. For the year, Communication Services was the winner, up 38.89%. Materials was the only negative sector for 2024, down 1.83%. In December, only three of the 11 GICS sectors increased. The index saw breadth decline dramatically, with only 54 issues up for the month.

The 10-year U.S. Treasury ended the month at a yield of 4.58%, up from 4.18% the prior month. The 30-year U.S. Treasury ended December at 4.78%, up from 4.48%. The Bloomberg U.S. Aggregate Bond Index returned -1.51%. The Bloomberg Municipal Bond Index returned -1.46%.

A new year gives you a new chance to review your goals. While New Year’s resolutions have something like a 90% failure rate, the changes you make to your investment plan may be more successful and lasting. The key? Don’t do it all at once.

Taking the time to review your situation, your budget, your income, your debt and most importantly – your goals – can help you make incremental changes that will work together to keep you on track.

Tying your goals to your finances can keep you focused, create motivation and momentum, and also impose discipline.

Laying out a roadmap of changes you need to make, and planning the optimum time for them is key. For example:

Combining personal goals, investments, and a view on the economy is at the core of what a financial advisor can bring to the table. We’re always here to help.

Curious about our other content? Check it out here.